Credit Inflation: How Borrowing Excess Devalues Financial Discipline

We live in a world where credit is everywhere. Want a new phone? Pay in 12 easy installments. Need groceries? Put them on a card. Thinking about a vacation? Just click “Buy now, pay later.” What used to be rare and deliberate — borrowing money — is now part of daily life. But there’s a deeper shift happening beneath the surface. As borrowing becomes normalized, it starts to reshape how we think about value, responsibility, and what it means to live within your means. This is credit inflation — not in interest rates, but in attitude. And its impact on financial discipline is more serious than it seems.

The Rise of Borrowing as a Lifestyle

Once, borrowing was tied to big decisions: buying a house, starting a business, paying for education. It was measured, often stressful, and always taken seriously. Today, borrowing is frictionless. One tap, one swipe, one approval — and you’re in debt. The line between affordability and availability has blurred. If you can get approved, you assume you can afford it. That shift encourages behavior that would’ve once been seen as reckless — now it’s just routine.

Easy Access, Shallow Reflection

With credit access expanding through mobile platforms, online lenders, and embedded financing, the barrier to borrowing is now nearly nonexistent. There’s no need to meet with a banker, explain your goals, or justify your choices. The loan is pre-approved, and the repayment terms are often buried in fine print. That ease removes a key part of financial discipline: pause. When borrowing takes effort, you think twice. When it doesn’t, you think less.

How Credit Rewards Impulsiveness

In a credit-inflated world, patience is punished. The person who saves is slower than the one who borrows. The saver waits, the borrower acts. And in many cases, the borrower appears to “win” — they get the product, the experience, the business opportunity, while others hold back. But what’s happening is a subtle shift in values. Planning becomes old-fashioned. Restraint is seen as hesitation. Impulse becomes synonymous with ambition. And short-term thinking takes priority over long-term stability.

The New Normal: Pay Later, Worry Never

Marketing plays a big role in pushing this mindset. “Buy now, pay later” doesn’t just describe a payment method — it signals that it’s okay to want something now and figure it out later. This message appears in shopping carts, airline sites, car dealerships, and even dental offices. Credit is no longer a tool; it’s a default. And that normalizes borrowing for everyday purchases that were once paid for in cash or not purchased at all.

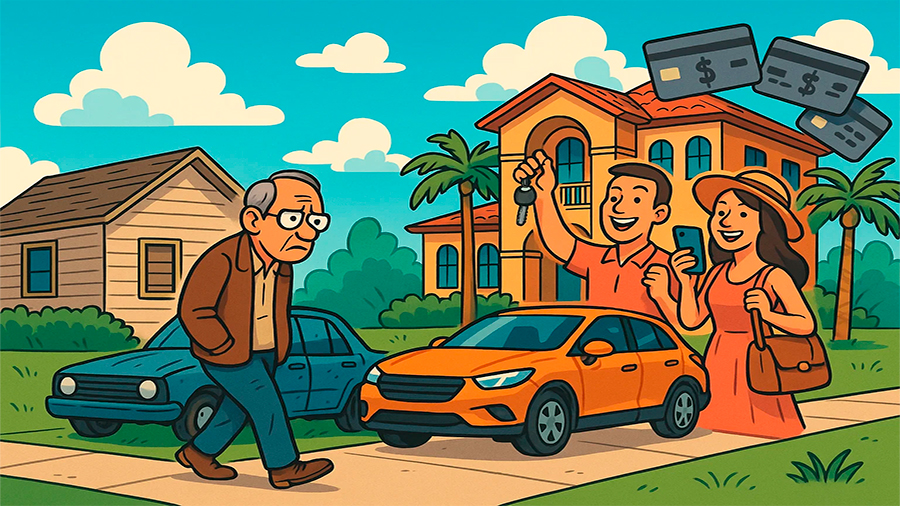

What Happens to People Who Play It Safe?

Ironically, the people who avoid debt — who wait, save, and plan — may end up feeling left behind. In a world of credit inflation, financial discipline can look like delay. You’re still driving the old car. You skipped the vacation. You passed on the latest phone upgrade. Meanwhile, your peers — the ones using credit — appear to be thriving. But their apparent lifestyle often hides a heavy burden: multiple monthly payments, high interest, and constant pressure to stay one step ahead of due dates.

The Invisible Cost of Credit Culture

Credit inflation doesn’t just impact individual choices — it changes the cultural baseline. Once enough people borrow, the economy adjusts. Prices go up. Companies know consumers will finance large purchases, so they push premium pricing. Subscription models, upgrades, extended plans — all are designed around long-term credit behavior. In the end, living without debt becomes harder, not easier. The person trying to stay out of debt finds fewer options, less flexibility, and higher upfront costs.

Discipline No Longer Feels Rewarded

One of the most damaging effects of credit inflation is that it breaks the link between discipline and progress. Saving up used to mean something. It was a path to ownership, security, and peace of mind. Now, saving feels slow — even obsolete. Why wait when everyone else is already enjoying what you’re working toward? This pressure can wear down even the most cautious person. When debt becomes the norm, discipline becomes the outlier.

Delayed Gratification vs. Instant Approval

There’s nothing exciting about waiting. But financial health often depends on exactly that — waiting until the money’s there, building a cushion, avoiding risky shortcuts. Credit inflation turns that strategy into a struggle. You have to justify patience while others are rewarded for urgency. That creates frustration. And in some cases, it pushes people to borrow just to “keep up,” even if they don’t really need or want the thing they’re financing. The result: more debt, more stress, and less clarity about what matters.

The Long-Term Risks of a Credit-First Economy

When too many people live on borrowed money, the entire system becomes fragile. Every debt relies on future income. Every payment plan assumes stability. But what happens when inflation rises, rates go up, or jobs become uncertain? Suddenly, the foundation cracks. The borrower’s lifestyle is no longer sustainable, and the lender tightens access. Defaults increase. Savings disappear. And those who once appeared to be ahead find themselves scrambling to recover.

From Personal Strain to Economic Exposure

Credit inflation isn’t just a personal finance issue — it’s systemic. If millions of consumers are overleveraged, small economic shocks can have outsized effects. Consumer spending slows, collections rise, and financial institutions start to pull back. The people who relied most on debt are hit first. But even those who managed responsibly may feel the ripple effects through higher prices, tighter credit, or fewer job opportunities as businesses respond.

Is There a Way Back to Discipline?

It’s not easy to swim against the current of credit normalization. But some are trying. Financial educators, debt-free influencers, and even fintech tools are pushing messages of awareness, intentionality, and limits. Budgeting apps, automated savings, and transparency tools help people understand how borrowing adds up. But real change also requires cultural support — recognizing that slow, stable growth is still valid. That not financing everything doesn’t mean falling behind. That saying “not now” is still a powerful financial move.

Rebuilding the Value of Restraint

We need to stop treating financial discipline as old-fashioned. It’s not about austerity — it’s about control. Living debt-free or borrowing strategically doesn’t mean giving up on opportunity. It means being deliberate. It means understanding the difference between affordability and approval. It means choosing a path that may be slower — but is far more stable when times get tough.

The Conclusion

Credit inflation has changed the financial landscape. Borrowing is no longer a rare decision — it’s a daily habit. But this constant access to easy money has hidden costs. It encourages impulsiveness, discourages savings, and erodes the sense of control that financial discipline once offered. While borrowing can still be useful, the culture around it needs a reset. We can’t let debt become the default — because when everything runs on credit, true financial strength starts to disappear.